.jpeg)

Sometimes, purchasing the right insurance for your property is not always as easy as we would wish it to be. In addition to choosing the best landlord policy for your rental property, you also have to differentiate what policy works best.

The most common policies you will see insurers quoting are DP1, DP2, and DP3. At first glance, these categories may seem straightforward enough, but the truth is these three types of policies and how they work can be surprisingly complicated. As a result, it is not uncommon to find property owners purchasing the wrong policy, especially when dealing with DP1.

What exactly is DP1, and why should you care? What does it cover, and when should you acquire it? What distinguishes it from other insurance plans? How do insurers determine compensation under this policy?

If you're looking for the answers to these questions, this article will help make sense of them.

A DP1 policy is a basic dwelling fire policy. It is common among property owners whose rental insurance would otherwise not cover the property in question. This will mostly touch on vacant units or standalone structures, like boat houses.

It is also referred to as a named perils policy, meaning it only protects you against damages from perils (aka risks) named in the policy. The insurance will not reimburse you if your house incurs damages from a peril not stated in the DP1 policy.

Another aspect that distinguishes the DP1 policy from the others is that it only pays the actual cash value (ACV) during a claim. That means it factors in the property's depreciation. So, your payout may be less than the property's actual replacement cost to repair or rebuild. . That’s because the older your house, the less value it has, at least according to the terms of a DP1 policy.

How does this work? Let’s say you have a rental unit needing a new roof due to a covered peril . The roof will cost you about $20,000, and the old one has been in place for 15 years. The expected lifespan of a roof with fiber cement shingles is about 25 years. You can calculate the actual cash value of your claim using the below formula:

In this example, you would receive $8,000 from your DP1 insurance policy. However, since the cost of a new roof is $20,000, you will be out of pocket for the remaining $12,000.

Nevertheless, some insurers provide replacement cost value (RCV), which does not factor in depreciation in the payout. It will, however, come at an additional cost. Since this option is not explicitly available, ensure you speak to your insurance agent to see whether it is possible to get it.

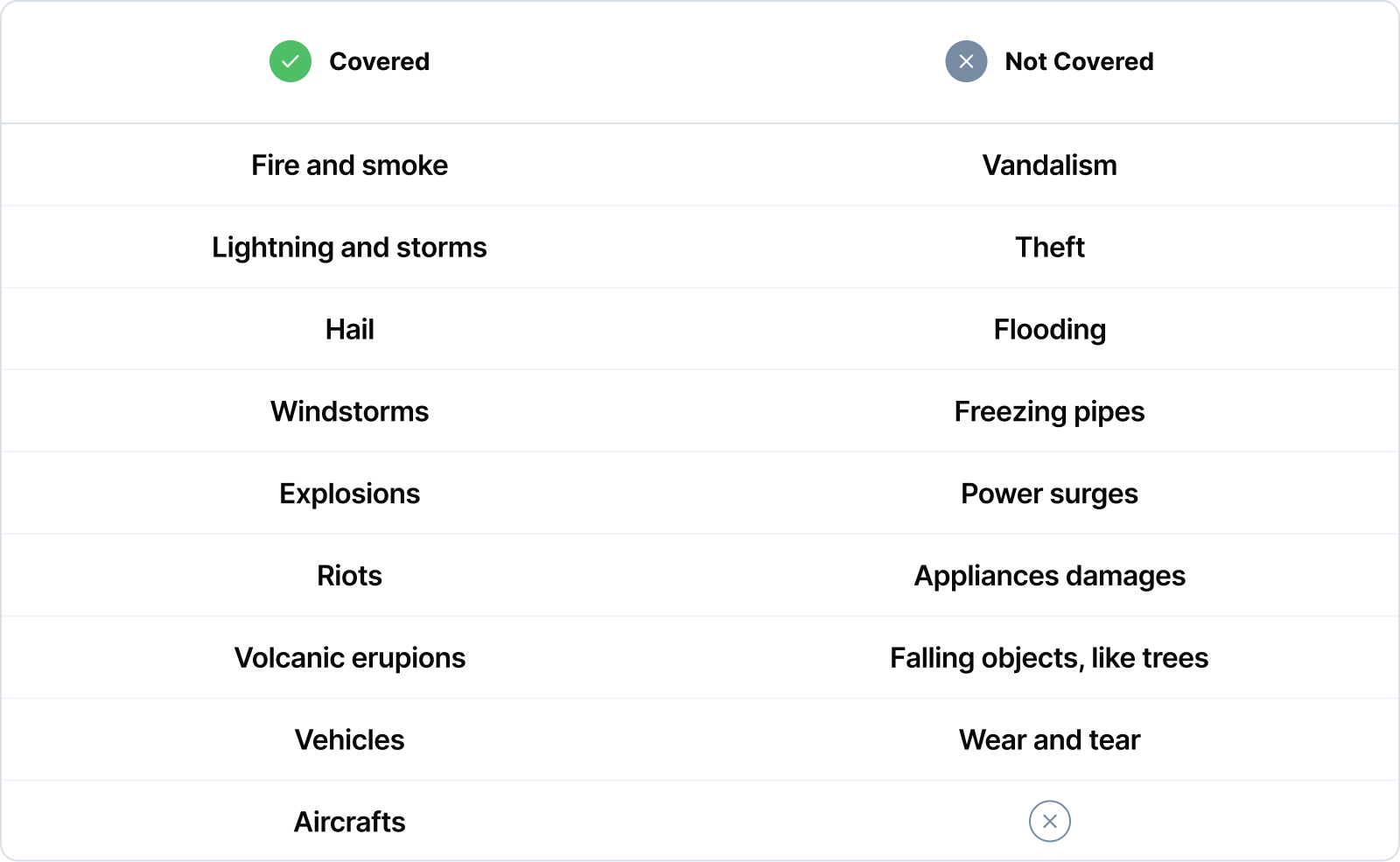

As stated, a DP1 policy is pretty basic, meaning it covers some of the most common perils, including:

In addition to these, a DP1 policy may also cover the property’s additional structures, like fences, garages, sheds, and personal property. However, some insurers do not cover additional structures, personal property, or liability. Those that do so may require an additional premium.

Although DP1 covers common perils, it doesn’t cover all of them unless otherwise stated in one’s policy, including

It is crucial for users to go through the provided policy and identify what perils are covered, which are excluded, and whether there is an allowance for additions before settling for any policy.

Considering that DP1 is a pretty basic policy with many exclusions of significant common perils, sometimes property owners question whether it is really necessary to have.

Here are a couple of situations where having a DP1 policy could be a good idea:

Perhaps you are waiting for tenants to move into your rental unit, which might take more than 60-90 days. Maybe you are left with an extra house after purchasing and moving into your new home. Or, perhaps, you inherited property and have put it on the market.

Whatever the reason, you can use a DP1 policy as long as that property sits vacant. Although the property is unoccupied so has no risk of tenant damages, it still faces risks from basic perils that DP1 covers.

This coverage ensures you are still protected against these common perils and won’t have to foot the bill for repairs.

It is always essential to have the best possible insurance coverage for your property, but landlords also have to conduct a cost-benefit analysis. A DP1 policy providing basic coverage is better than leaving a rental property uninsured.

However, if you choose this insurance option, remember it is only basic. Any damages that might arise and are excluded from your policy will be yours to bear. And that’s a financial risk that could be higher than it would have cost for a better policy.

Apart from DP1, two other policies to consider are DP2 and DP3. Like DP1, the DP2 policy is also a named peril policy. The main difference is that it offers protection against more common perils than the DP1 policy. By comparison, the DP3 policy is an open perils policy. It covers damages against all risks unless otherwise stated (or specific exclusions).

DP1 is also a more affordable option than DP2 and DP3. A DP3 is the most expensive policy. In addition, both the DP2 and DP3 provide replacement cost value (RCV) where the insurer doesn’t deduct the property’s depreciation from your claim (Note: in some DP2 and DP3 policies for certain roof ages, roofs may be covered for ACV rather than RCV while the rest of the house will be covered for RCV).

One of the most effective ways to find the right policy is to hire a professional insurance broker who has access to industry-best rates for rental property and casualty plans, ensuring that your assets are protected. Insurance brokers also have a fiduciary duty to you, which means they are legally required to put your interests ahead of those of the insurance companies.

An alternative route is to contact other real estate investors. Hearing about others' experiences may help you determine whether the insurer pays claims on time.

Another popular method for real estate investors to locate the right insurance for their property is Obie. Obie can help you get a landlord insurance estimate and inexpensive, transparent coverage entirely online. There are no paper applications to fill out or lengthy waiting periods.

Answer a few basic questions to get the appropriate insurance and coverage for single-family rental properties, multifamily structures with two to four units, and condominiums based on your specific requirements. On average, landlords are saving 25% with Obie.

Go here to get an instant quote today.

In conclusion, the DP1 policy is your go-to coverage if you have a tight budget, have a vacant house. It is a basic policy covering a few common perils, like lightning, fire and smoke, windstorms, hailstorms, and explosions.

Due to its exclusion of some common perils, like theft, vandalism, and flooding, DP2 or DP3 policies may be better if you have the budget for additional insurance coverage.

Before settling on a specific policy, it's advisable to understand the common perils covered and those excluded. Remember that claims with a DP1 policy are paid based on the actual cash value. So, if your rental property is older, you may pay more out of pocket once depreciation is factored in.

AK #3001323846

AL #3000908445

AR #3000916052

AZ #3000916073

CA #6002583

CO #648689

CT #2716551

DC #3001009541

DE #3001247094

FL #L109506

GA #213072

HI #534451

IA #3000916206

ID #838797

IL #3001410691

IN #3563275

KS #845129262-000

KY #1091384

LA #863278

MA #2141684

MD #3000916120

ME #AGN378956

MI #128349

MN #40736335

MO #3000915661

MS #15040365

MT #3001247095

NC #1000712051

ND #3001247091

NE #3001266894

NH #3001152116

NJ #3001232518

NM #3002380649

NV #3562275

NY #1638380

OH #1313308

OK #3000916108

PA #953805

PA #1027420

PA #1038898

RI #3001151816

SC #3000916142

SD #10027388

TN #3001140087

TX #2538944

UT #819412

VA #148902

VT #3653729

WA #1101235

WI #3000916141

WV#3001232811

WY #460662

AZ #3001495975

CA #6006652

CO #709122

FL #L114608

IL #3001410691

IN #3715685

IN #3726236

MD #3001485673

MI #134516

NJ #3001475592

NV #3715355

NV #3733855

OH #1389553

OH #1396167

OR #3001525732

PA #1027420

PA #1038898

TN #3001475594

TX #2720237

TX #2722701

UT #886292

UT #886293

VA #152131

WI #3001475580

.jpg)

.jpg)

.jpg)